March 10, 2022

Written By: Andrew Hallam

There are several physical laws. Some examples include the law of gravity, the law of friction, and the ever-scintillating Pascal’s law, which relates to water pressure. Physical laws are undeniable truths. While it isn’t a physical law, there should be a law based on the irrefutable premise that index funds always beat most actively managed funds.

This isn’t news to most investors. But most people don’t know why indexes win. They just know the following:

1. Index funds beat most actively managed funds when stocks fall.

2. Index funds beat most actively managed funds when stocks rise.

3. Actively managed mutual funds that are fortunate enough to beat index funds over one measured time period typically “revert to the mean.” This means they soon underperform.

You might believe index funds beat most actively managed funds because index funds incur lower costs. That’s true, but it doesn’t answer the question, “Why do these lower costs increase the odds that indexes win?”

If this “law” had a name, it might be the “Sharpe Law,” named after the Nobel Prize-winning economist, William F. Sharpe. In his research paper, The Arithmetic of Active Management, he asserted that the stock market’s return in any given year is equal to the return of all professionally managed money invested in that given market. For example, if the US stock market gained 5 percent this year, the aggregate return of all professionally managed money in US stocks would be 5 percent, before fees. As a group, they would earn the market’s return on their stocks because they represent the money that’s invested in the market.

In other words, if we identified the “owner” of every share in the market, these owners would represent the investors in all actively managed funds, day-traders, individual stock owners, institutional traders, pension funds, hedge funds, and…index fund investors. If the market gained 5 percent, the pre-fee return of indexes and the sum of active management in that market would be 5 percent. That’s as irrefutable as a law of physics.

After trading fees and expense ratio costs, actively managed funds must fall behind because they charge higher fees than index funds.

However, there’s a nuance worth pointing out. Most active fund managers keep a component of cash in their accounts. So, while the aggregate return of all active management would earn the market’s return on their funds’ stock market component, their funds might post a slightly higher return than the stocks they own when stocks fall. For example, assume all actively managed mutual funds had 20 percent of their fund’s value in cash in 2008. When stocks fell 37 percent, their aggregate return on US stocks would have been minus 37 percent, before fees. But if they had 20 percent in cash, that portion of their fund wouldn’t have lost value.

This might sound like an argument for active management during down markets. And it would be if it weren’t for three things:

- Nobody knows when stocks will fall, so fund managers don’t know when to stockpile cash. Those who guess right once typically guess wrong the next time.

- Because such consistent predictions are almost impossible, the vast majority of actively managed funds still underperform their benchmark indexes when stocks drop. For example, according to SPIVA, 64.23 percent of US actively managed stock market funds lost to the US index when stocks crashed in 2008.

- When active funds keep money in cash, their funds don’t rise as strongly when stocks rise…because their cash slows them down.

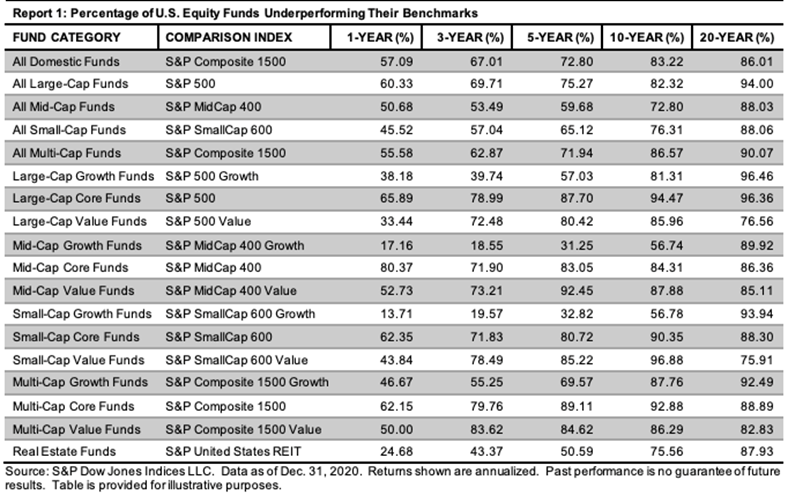

Over full market cycles, an ever-increasing percentage of actively managed funds lose to their benchmark indexes. For example, over the past 20 years, we had several market cycles. Stocks fell in 2001 and 2002. Stocks gained ground from 2003to 2007. They fell hard in 2008 and rose strongly almost every year from 2009to 2020. As shown in the table below, over the 20 years ending December 31, 2020, (see the far right column) the vast majority of actively managed funds underperformed their benchmark indexes. For example, 94 percent of actively managed large-cap funds underperformed the S&P 500.

This will always be the case, much like a physical law of gravity or friction. That’s because the aggregate return of all professionally managed money in the stock market will always be the same return as the stock market itself…before fees. After fees, active management must lose to the market.

That’s the law.

Andrew Hallam is a Digital Nomad. He’s the author of the bestseller Millionaire Teacher and Millionaire Expat: How To Build Wealth Living Overseas

This article and or podcast contains the opinions of the author but not necessarily the opinions of AssetBuilder Inc. The opinion of the author is subject to change without notice. All materials presented are compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This article is distributed for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.

Performance data shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown.

AssetBuilder Inc. is an investment advisor registered with the Securities and Exchange Commission. Consider the investment objectives, risks, and expenses carefully before investing.